The traditional reliance upon standard statutory audits as a primary defense against malfeasance is, in the contemporary landscape of multi-jurisdictional mandates, a precarious strategy that often overlooks the nuanced indicators of sophisticated financial instrument fraud; consequently, the integration of forensic accounting for fraud detection has transitioned from a reactive necessity to a cornerstone of institutional capital preservation. You likely recognize that as fraud schemes become increasingly opaque, particularly following the 62% rise in check fraud losses reported by institutions as of early 2026, the margin for error in safeguarding high-value interests has effectively vanished.

This article provides the clarity required to master the sophisticated methodologies utilized by Tier-1 experts to identify irregularities and secure institutional capital within complex cross-border mandates. We’ll examine the transition toward effectiveness-based regulatory compliance, the strategic application of advanced data analytics, and the rigorous validation protocols essential for confirming the legitimacy of financial instruments. Through this institutional framework, you’ll gain the intellectual depth needed to mitigate hidden liabilities and align your risk management with the highest professional standards of precision and discretion.

Key Takeaways

- Discern the critical distinction between standard sampling audits and the exhaustive factual validation provided by forensic accounting for fraud detection within institutional mandates.

- Master the deployment of advanced analytical protocols, such as Benford’s Law, to identify sophisticated irregularities in multi-jurisdictional financial reporting.

- Recognize the necessity of on-ground verification services to confirm the physical legitimacy of assets and collateral, moving beyond purely digital due diligence.

- Implement a structured framework for complex project management that integrates forensic oversight into every financial deliverable and milestone.

- Leverage the expertise of seasoned banking professionals to ensure regulatory compliance and the long-term preservation of institutional capital.

Forensic Accounting vs. Standard Auditing: Defining Institutional Precision

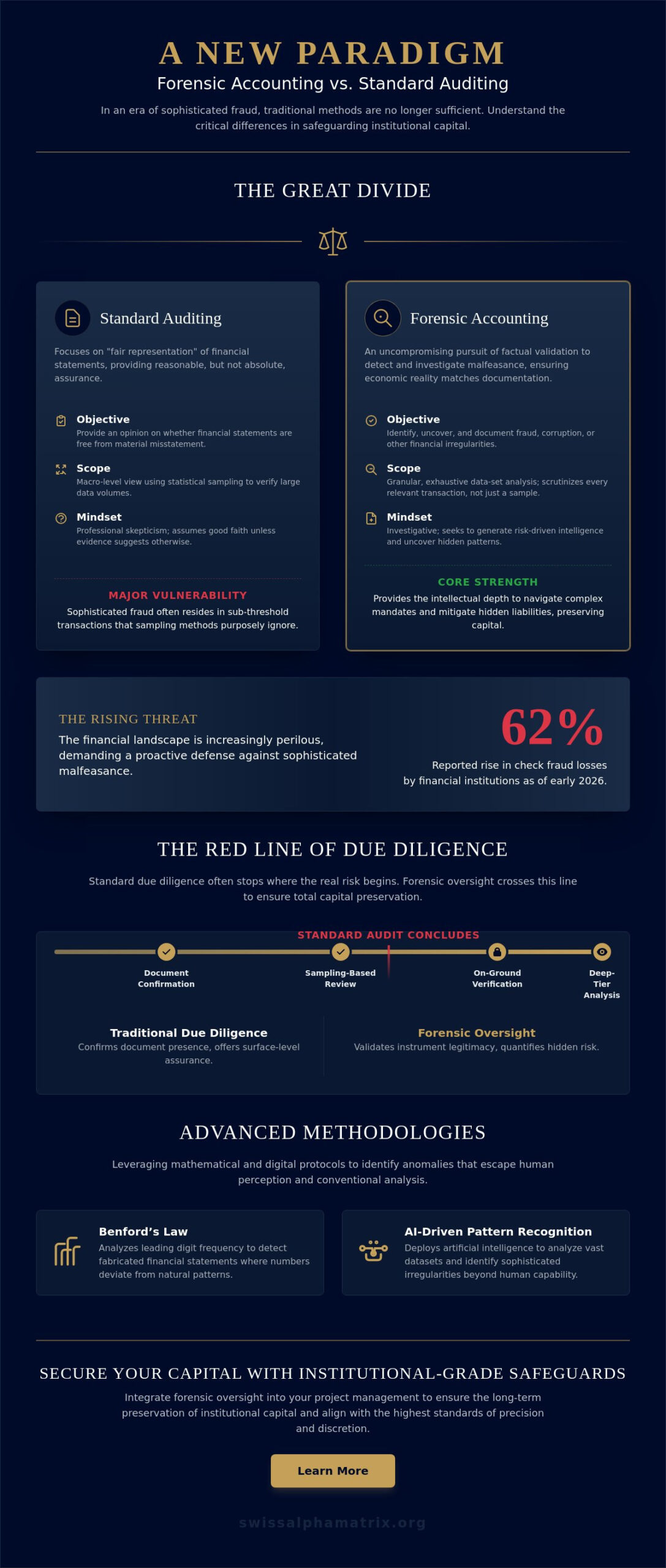

The fundamental divergence between a standard statutory audit and forensic accounting lies in the ultimate objective of the engagement, which, for the former, centers on providing reasonable assurance that financial statements are free from material misstatement, whereas the latter demands an uncompromising pursuit of factual validation. Traditional audits operate under a framework of “fair representation” that often relies upon statistical sampling to verify large volumes of data. In the high-stakes environment of institutional capital deployment, such a macro-level view is increasingly viewed as insufficient. As we move through 2026, the industry is witnessing a definitive transition from these sampling-based reviews to exhaustive data-set analysis. This shift is driven by the realization that sophisticated fraud often resides within the sub-threshold transactions that standard materiality levels purposely ignore, necessitating a more granular approach to protect institutional interests.

Within this framework, the forensic accountant emerges not merely as a technician, but as a strategic advisor essential to capital deployment decisions. By identifying the subtle indicators of financial manipulation that a standard audit might overlook, these experts provide the intellectual depth required to navigate complex mandates. Forensic accounting for fraud detection ensures that the underlying economic reality of a deal matches its surface-level documentation, providing a level of certainty that is indispensable for long-term preservation and strategic growth.

The Threshold of Investigative Skepticism

An investigative mindset transcends the basic professional skepticism required by standard accounting principles; it requires a profound understanding of how anomalous patterns in institutional ledger entries can signal deep-seated structural irregularities. Forensic experts don’t merely check for compliance. They generate risk-driven intelligence by scrutinizing the underlying logic of a transaction rather than just its external documentation. For entities managing multi-jurisdictional mandates, this level of scrutiny is the only way to ensure that reported figures reflect actual performance metrics rather than creative accounting maneuvers.

When Standard Due Diligence Is Insufficient

Traditional M&A due diligence often fails to protect capital when dealing with complex financial instruments or opaque offshore structures, as there is a distinct “red line” where standard procedures conclude while the actual risk remains unquantified. In mandates involving bank-guaranteed instruments, for example, a standard audit might confirm the presence of a document; however, it won’t necessarily verify the instrument’s legitimacy through audit-grade validation. Forensic accounting for fraud detection fills this void by performing on-ground verification and deep-tier background analysis. By integrating forensic oversight into complex project management, institutions can move beyond the “check-the-box” methodology, ensuring total capital preservation through every phase of the investment lifecycle.

Advanced Methodologies for Detecting Multi-Jurisdictional Financial Fraud

The identification of malfeasance within complex, cross-border mandates necessitates a shift from surface-level observation to the application of advanced mathematical and digital protocols. Benford’s Law, which analyzes the frequency distribution of leading digits, remains a cornerstone for detecting fabricated financial statements where human-generated numbers inevitably deviate from natural patterns. In the current 2026 landscape, where over 85% of financial firms have integrated artificial intelligence, the role of Uncovering Fraud and Protecting Organizations through AI-driven pattern recognition has become indispensable for identifying anomalies that escape human perception. These tools allow for the “Follow the Money” protocol to be executed with surgical precision, tracing beneficial ownership through opaque offshore jurisdictions and intricate trust structures that are designed to obscure the true origin of capital.

Specialized practitioners also focus on identifying “Circular Funding” schemes, which are frequently observed in high-value infrastructure projects where funds are cycled through various entities to create an illusion of liquidity or to satisfy equity requirements artificially. Detecting these loops requires an exhaustive analysis of inter-company transfers across multiple jurisdictions. For institutions seeking to maintain a defensive posture, establishing a robust Risk Management Framework is the most reliable method for ensuring that these sophisticated patterns are identified before capital is irrevocably committed.

Digital Forensics and Transactional Reconstruction

In scenarios involving distressed assets or entities with compromised records, digital forensics becomes the primary tool for recovery. Transactional reconstruction is the process of rebuilding a financial timeline from disparate data points. By utilizing blockchain forensics to verify modern capital flows and employing advanced recovery techniques for deleted financial data, experts can restore transparency to even the most fragmented ledgers. This process is essential for verifying that the historical performance metrics presented during due diligence are rooted in verifiable economic activity.

Detecting Institutional Instrument Fraud

The validation of high-value bank instruments, such as Standby Letters of Credit (SBLCs) and Bank Guarantees, requires a specialized subset of forensic expertise that standard auditors rarely possess. Red flags often include inconsistent SWIFT message formatting, unauthorized signatory patterns, or the use of non-standard verbiage that deviates from ICC standards. To mitigate multi-million dollar exposure, institutions should utilize dedicated bank instrument validation services. These services go beyond document review, employing direct bank-to-bank inquiries and on-ground verification to ensure the instrument is both authentic and fully funded within the issuing jurisdiction. Forensic accounting for fraud detection in this context serves as the final, uncompromising filter against the sophisticated deception often found in cross-border financial instruments.

The Criticality of On-Ground Verification in Forensic Mandates

Digital validation, while essential for tracing modern capital flows, represents only half of a comprehensive forensic mandate; the remaining half necessitates physical, on-ground verification to dismantle the “paperwork mirage” often employed by sophisticated actors. These fraudsters excel at constructing convincing, yet entirely non-existent, corporate histories through digital manipulation and coordinated shell company filings across multiple jurisdictions. To counter such deception, forensic accounting for fraud detection must move beyond the ledger and into the physical realm. The “Physical Asset Audit” serves as the ultimate arbiter of truth, confirming that the collateral, whether it be precious metals in a Geneva vault or specific inventory in a London warehouse, actually exists within the claimed jurisdiction and is under the legal control of the counterparty.

In global financial hubs such as Hong Kong or Zurich, the Role of Forensic Accountants in Fraud Investigations extends to performing discreet inquiries that no algorithm can replicate. These professionals engage with local registers, verify active site operations, and interview third-party stakeholders to ensure that the institutional image presented to investors isn’t merely a digital facade. This level of scrutiny identifies red flags that standard audits miss, including:

- Discrepancies between digital records and physical inventory counts during unannounced site visits.

- Key personnel who, despite impressive digital profiles, lack verifiable professional histories or physical presence at operational headquarters.

- Operational sites that lack the necessary infrastructure, staffing, or utility consumption required for their claimed industrial activities.

Operational Due Diligence Beyond the Balance Sheet

Effective risk mitigation requires a profound assessment of the human element behind the capital. This involves verifying the credentials of key personnel and scrutinizing their past performance in high-stakes mandates to ensure alignment with institutional standards. By mastering cross-border investment due diligence, experts can assess a counterparty’s “culture of compliance” through on-site operational reviews. This process identifies whether a firm’s internal controls are functional or merely ornamental, providing a clearer picture of the underlying operational risk.

Mitigating Counterparty Risk in Opaque Markets

In markets characterized by low transparency, a “boots on the ground” approach is the only reliable method for verifying international joint venture partners. It’s not uncommon to encounter “phantom offices” where a prestigious address leads only to a shared mailroom with no actual operational staff. Physical surveillance and site visits allow forensic teams to identify these shell operations before they compromise the mandate. Ultimately, this on-ground intelligence informs the final risk assessment, providing executive stakeholders with the intellectual depth and professional calm needed to ensure total capital preservation.

Integrating Forensic Oversight into Complex Project Management

The transition from preliminary due diligence to active project execution represents a critical juncture where capital is often most vulnerable to erosion; therefore, the integration of forensic accounting for fraud detection into a structured project management framework is essential for maintaining institutional control. Rather than treating forensic review as a post-mortem exercise, sophisticated entities establish an independent Project Management Office (PMO) equipped with forensic capabilities from the project’s inception. This proactive architecture ensures that every financial milestone is validated against factual economic reality before any further capital deployment occurs. A disciplined approach to this integration follows five primary strategic steps:

- Step 1: Establishing an independent PMO that operates outside the influence of transaction originators to ensure entirely objective verification.

- Step 2: Defining a “Deliverable Review Matrix” which subjects every financial reporting milestone to rigorous forensic scrutiny before funds are released.

- Step 3: Implementing continuous monitoring protocols that analyze real-time data flows, effectively replacing the inherent inadequacy of periodic spot checks.

- Step 4: Utilizing a RACI matrix to define clear roles and ensure absolute accountability for every financial oversight task.

- Step 5: Establishing direct, confidential reporting lines to the Board of Directors or the Family Office Principal to prevent any filtering of critical risk intelligence.

The Role of Independent Project Oversight

Objectivity remains the hallmark of effective capital protection. Project managers must remain entirely separate from the transaction originators, as this independence prevents the cognitive biases or conflicts of interest that often lead to the overlooking of subtle red flags. Understanding the strategic architecture of independent financial project management allows institutions to build a robust firewall against capital erosion. By managing stakeholder expectations through a prism of objective data, the forensic team ensures that the project’s financial integrity remains uncompromised by the pressures of deal velocity.

Regulatory Compliance and Forensic Reporting

Forensic findings must be prepared to audit-grade standards, ensuring they can withstand the intense scrutiny of potential litigation or formal regulatory inquiries. This requires a profound understanding of evolving international financial regulations, particularly as jurisdictions shift toward effectiveness-based AML programs. Maintaining Swiss-level discretion while fulfilling global obligations ensures that sensitive mandates are managed with the utmost privacy and technical precision. To secure your interests through a dedicated Risk Management Framework, it’s essential to partner with experts who prioritize long-term preservation over short-term speculation.

Swiss Alpha Matrix: Institutional-Grade Safeguards for Capital Preservation

The efficacy of any protective framework is fundamentally tethered to the calibre of its architects; consequently, Swiss Alpha Matrix distinguishes itself through a “Tier-1” pedigree, drawing upon the collective expertise of former senior banking executives who possess an intimate understanding of global capital markets. This background provides a superior level of forensic insight that transcends traditional accounting, as it is rooted in the practical realities of high-stakes institutional finance and the intricate mechanics of complex project management. By integrating forensic accounting for fraud detection with the traditional values of Swiss discretion and regional precision, we offer a methodology that is both technically exhaustive and professionally refined. This approach ensures that every mandate, from audit-grade instrument validation to on-ground verification services, is conducted with a sense of quiet authority and technical precision that mirrors the standards of high-end private wealth management.

Our commitment to protecting the principal is absolute, manifesting in an advisory style that remains unemotional and strictly evidence-based, prioritizing long-term preservation over short-term speculation. In an environment where sophisticated financial instrument fraud has become increasingly prevalent, as evidenced by the 62% increase in check fraud losses reported in early 2026, the need for a seasoned partner who can identify subtle red flags is paramount. We view ourselves not merely as a service provider but as a dedicated partner, positioning our master planners to navigate the intricate dynamics of cross-border mandates with a focus on stability and trust.

Tailored Mandates for Sophisticated Stakeholders

Standardized, “off-the-shelf” forensic services frequently prove inadequate when applied to complex, multi-billion dollar environments where the risks are as unique as the transactions themselves. Swiss Alpha Matrix prioritizes hyper-personalization, developing bespoke risk mitigation frameworks that address the specific vulnerabilities of each mandate with meticulous attention to detail. In cross-border instrument validation mandates, for instance, we move beyond digital checks to perform exhaustive on-ground inquiries, ensuring that the underlying collateral and counterparty histories are fully verified before any institutional capital is committed, thereby preventing exposure to non-existent corporate histories.

Securing Your Financial Future

The transition from financial uncertainty to “audit-grade” confidence requires a structured, logical progression from broad philosophical principles down to specific strategic pillars. Engaging Swiss Alpha Matrix for a discreet preliminary risk assessment allows stakeholders to identify potential liabilities and hidden risks before they escalate into systemic failures. We invite you to secure your next mandate with institutional-grade financial advisory methodologies, ensuring your interests are managed by experts who value privacy, exclusivity, and the intellectual depth required for total capital preservation.

Architecting Strategic Resilience Through Institutional Oversight

The preservation of institutional capital in a landscape defined by increasing complexity requires a definitive departure from passive compliance toward a proactive, investigative framework. By prioritizing absolute factual validation over mere fair representation and ensuring that digital records are anchored by rigorous on-ground verification, entities can effectively dismantle the sophisticated mirages created by modern actors. The integration of forensic accounting for fraud detection into the core of project management provides the intellectual depth necessary to mitigate hidden liabilities before they compromise a mandate.

Led by former Tier-1 global bank executives, Swiss Alpha Matrix delivers a standard of precision rooted in historical reliability and regional excellence. Our methodology leverages audit-grade instrument validation protocols and global on-ground verification capabilities to ensure your interests remain in the hands of seasoned, unemotional experts who prioritize long-term stability. To secure the strategic growth of your assets through a bespoke risk management framework, we invite you to consult with our senior partners on your complex financial mandate. Establishing this level of professional calm is the definitive step toward achieving total capital preservation in an evolving global market.

Frequently Asked Questions

What is the primary difference between forensic accounting and a standard financial audit?

Standard audits aim to provide reasonable assurance that financial statements are free from material misstatement, whereas forensic accounting for fraud detection seeks absolute factual validation of specific transactions. While an auditor utilizes sampling to assess “fair representation,” a forensic expert performs exhaustive analysis to identify intent and malfeasance. This specialized approach is essential for mandates where high-value interests require a level of certainty that standard statutory reviews simply cannot provide.

How long does a typical forensic accounting investigation for fraud detection take?

The duration of a forensic mandate varies significantly based on the complexity of the financial instruments and the number of jurisdictions involved. A focused validation of a specific bank instrument may conclude within several business days; however, a comprehensive reconstruction of multi-year transactional timelines for distressed assets can extend over several months. Each engagement is tailored to the specific strategic pillars of the mandate to ensure that thoroughness is never sacrificed for unseemly haste.

Can forensic accounting be used proactively during a merger or acquisition?

Forensic accounting is increasingly utilized as a proactive mechanism during the operational due diligence phase of mergers and acquisitions to identify hidden liabilities. Rather than a reactive “post-mortem,” this application serves as an institutional safeguard that verifies the legitimacy of assets and the accuracy of performance metrics before capital is committed. It provides the intellectual depth required to distinguish between genuine strategic growth and creative accounting maneuvers designed to inflate valuation.

What are the most common red flags that trigger a forensic accounting mandate?

Common indicators that necessitate a forensic mandate include anomalous patterns in institutional ledger entries, lack of transparency regarding beneficial ownership, and inconsistencies in SWIFT message formatting. The discovery of “phantom offices” or a counterparty’s refusal to allow on-ground verification of physical collateral often signals deeper structural irregularities. Identifying these red flags early through specialized oversight is a cornerstone of effective risk management and long-term capital preservation.

How do forensic accountants verify the legitimacy of international bank instruments?

Verification of international bank instruments, such as SBLCs or Bank Guarantees, involves a multi-layered protocol that includes SWIFT MT760 analysis and direct bank-to-bank inquiries. Forensic accounting for fraud detection in this context also requires on-ground verification to confirm the issuing entity’s operational legitimacy and the instrument’s funding status. This rigorous process ensures that the financial instruments utilized in complex mandates are both authentic and legally enforceable across borders.

Is forensic accounting evidence admissible in international arbitration or court proceedings?

Forensic findings are frequently utilized in international arbitration and court proceedings, provided they meet “audit-grade” standards and comply with the specific evidentiary requirements of the relevant jurisdiction. While we don’t provide legal representation, our reports are structured to provide the factual clarity and technical precision necessary for legal counsel to mount a robust argument. Maintaining this standard of technical accuracy ensures that findings remain a reliable anchor during complex cross-border disputes.

How does Swiss Alpha Matrix maintain discretion during high-stakes investigations?

Swiss Alpha Matrix maintains the highest standards of discretion by utilizing direct, confidential reporting lines to the Board of Directors or Family Office Principals. Our team, comprised of former Tier-1 banking executives, understands that privacy is a non-negotiable requirement for sophisticated stakeholders. By operating with a sense of quiet authority and avoiding the frantic energy of less specialized firms, we ensure that sensitive investigations remain entirely confidential and secure.

What role does digital forensics play in modern institutional fraud detection?

Digital forensics is the primary mechanism for reconstructing transactional timelines and verifying modern capital flows through complex data sets. It utilizes advanced pattern recognition and blockchain analysis to identify anomalies that escape traditional review methods. In the contemporary landscape, where over 85% of financial firms have integrated artificial intelligence as of 2025, digital forensics provides the technical depth required to dismantle sophisticated schemes and ensure that every financial deliverable is rooted in verifiable data.