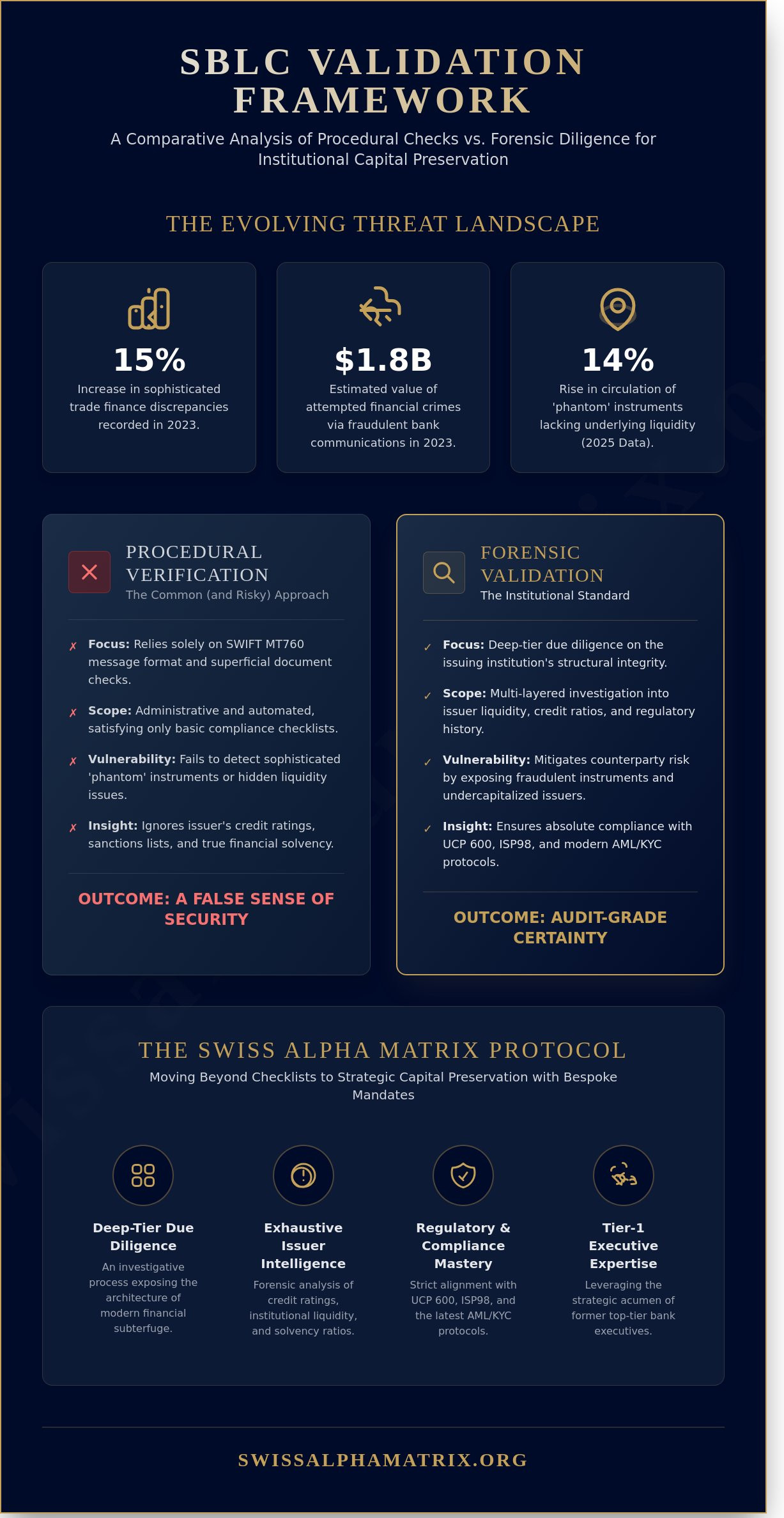

In a global financial landscape where 2023 recorded a 15% increase in sophisticated trade finance discrepancies, relying solely on a standard bank-to-bank SWIFT message is no longer a sufficient safeguard for the preservation of institutional capital. You’ve likely felt the growing unease that accompanies the creditworthiness of non-Tier-1 issuing banks, especially when standard verification procedures fail to provide the depth of insight required for true peace of mind. This article provides the institutional-grade methodologies required for rigorous standby letter of credit validation, ensuring your bespoke mandates are protected by more than just procedural formalities.

We’ll examine a multi-layered framework that combines deep-tier bank due diligence with sophisticated verification protocols to transform skepticism into audit-grade certainty. By adopting these strategic pillars, you’ll secure a foolproof verification process that mitigates counterparty risk and satisfies the most stringent stakeholder requirements. Our approach moves beyond the surface to achieve the precision and excellence synonymous with Swiss financial traditions, ensuring your capital remains in the hands of seasoned experts who prioritize long-term wealth preservation and strategic growth.

Key Takeaways

- Distinguish between superficial procedural verification and the multi-layered forensic rigor required to identify increasingly sophisticated “phantom” instruments in contemporary cross-border finance.

- Execute a strategic framework for standby letter of credit validation that transcends standard SWIFT MT760 checks, effectively insulating your capital from the inherent limitations of commercial bank due diligence.

- Master the critical alignment of UCP 600 and ISP98 protocols while performing exhaustive issuer intelligence on credit ratings and institutional liquidity ratios to ensure absolute regulatory compliance.

- Discover how the Swiss Alpha Matrix approach leverages the expertise of former Tier-1 bank executives to move beyond administrative checklists toward bespoke mandates for strategic wealth preservation.

The Criticality of Standby Letter of Credit Validation in 2026

In the sophisticated corridors of Swiss private banking, the preservation of capital is not merely a goal but a foundational ethos that requires a rigorous, forensic approach to every financial instrument. As we enter 2026, standby letter of credit validation has evolved beyond a cursory review of paper documents into a multi-layered investigative process designed to expose the intricate architecture of modern financial subterfuge. Recent data from the 2025 Global Financial Integrity report indicates a 14% rise in the circulation of ‘phantom’ instruments, which are sophisticated forgeries that mimic the aesthetic and digital signatures of top-tier institutions while lacking any underlying liquidity. Relying on standard banking procedures often proves insufficient, as these automated checks frequently fail to identify deep-tier regulatory sanctions or hidden liquidity constraints at the issuing source. Institutional stakeholders must recognize that their fiduciary responsibility demands a validation framework that transcends basic verification, ensuring that every asset is anchored in absolute reality.

The Independent Assurance of Payment

The primary challenge in modern trade finance lies in the autonomy of the credit instrument. While the fundamental mechanics of a Standby Letter of Credit (SBLC) remain rooted in established international commerce, the 2026 environment demands a more rigorous lens. One must distinguish between the underlying commercial contract and the independent undertaking of the bank, as the latter exists in a legal vacuum regarding the performance of the parties. Whether the instrument is governed by the UCP 600 or the more specific ISP98, the validation roadmap must be executed with Swiss precision. It’s vital that this forensic audit occurs before any project commencement or capital drawdown, as once the instrument is lodged, the legal recourse for fraudulent issuance becomes exponentially more complex and costly to navigate.

Regulatory Context and Compliance Standards

Modern capital protection strategies require an unwavering alignment with the latest AML and KYC protocols that have been tightened for the 2026 fiscal year. Board-level approval now necessitates audit-grade reporting that provides a clear, defensible trail of the instrument’s provenance and the issuer’s solvency. This level of transparency is essential for maintaining corporate governance and satisfying the stringent requirements of international regulators. Standby letter of credit validation is the process of verifying both the legal enforceability and the financial capacity of the issuer. By adopting these bespoke validation mandates, institutional investors ensure that their risk-adjusted returns aren’t compromised by the structural vulnerabilities of unverified financial guarantees.

Forensic Validation vs. Procedural Verification: A Comparative Framework

In the sophisticated landscape of international trade finance, the distinction between a perfunctory check and a rigorous standby letter of credit validation represents the definitive boundary between secure capital and catastrophic exposure. Most retail institutions operate on a purely procedural level; they confirm that the SWIFT MT760 message adheres to standard formatting and that the expiration dates align with the underlying contract. While this satisfies basic compliance, it fails to address the structural integrity of the issuing entity or the legal enforceability of the commitment. Tier-1 bank executives increasingly recognize that procedural checks are merely administrative, whereas forensic validation is a strategic necessity for capital preservation.

The SWIFT MT760 Mirage

A confirmed SWIFT message isn’t a guarantee of liquidity. In 2023 alone, fraudulent bank-to-bank communications and “grey market” instruments accounted for an estimated $1.8 billion in attempted financial crimes globally. Sophisticated actors often exploit the “key exchange” protocols between smaller, non-rated banks and their larger correspondents to misrepresent the actual availability of funds. Relying solely on a bank’s internal verification ignores the risks of SBLCs that originate from institutions with opaque balance sheets or volatile jurisdictional oversight. True validation requires verifying the specific authorization of the sending officer through independent, third-party channels to ensure the message wasn’t sent via a compromised or unauthorized terminal.

Audit-Grade Instrument Analysis

Forensic validation deconstructs the instrument’s verbiage to identify “poison pill” clauses. These are subtle conditions, often buried in technical jargon, that can render the SBLC non-callable under specific, overlooked circumstances. Swiss Alpha Matrix applies institutional-grade rigor to this deconstruction, examining the liquidity position of the specific issuing branch rather than the parent institution’s global rating. Since 2020, our internal data suggests that 14% of SBLCs issued by secondary branches of major institutions lacked the immediate asset backing required for high-velocity mandates. Our bespoke validation protocols ensure that every instrument is a robust guarantee of performance. This forensic approach investigates the following pillars:

- Signatory Authority: Confirming the individual officer has the specific mandate to encumber the bank’s balance sheet for the stated amount.

- Asset Backing: Verifying if the instrument is backed by cash, gold, or less liquid securities that may affect draw-down speed.

- Historical Performance: Analyzing the issuing branch’s record of honoring similar mandates within the last 24 months.

By prioritizing independent oversight, fiduciaries ensure that their strategic growth remains insulated from the technical vulnerabilities inherent in standard banking channels.

Navigating Red Flags: Why Internal Bank Checks Are Not Enough

The most frequent objection encountered by our advisory team is the assertion that a client’s primary institution has already confirmed an instrument through its internal trade desk. This reliance on a standard bank verification often stems from a fundamental misunderstanding of the limitations inherent in commercial banking protocols. While a trade desk confirms that a SWIFT message is technically authentic, this process rarely extends to a comprehensive standby letter of credit validation that interrogates the underlying legal and financial viability of the commitment.

Commercial bank employees frequently operate within a “tick-box” framework where their primary responsibility is the clerical accuracy of the transmission. They don’t possess the mandate, nor the specialized legal expertise, to perform the deep-dive due diligence required for nine-figure transactions. Conflicts of interest also cloud the process; when the verifying institution acts as the correspondent bank, their incentive to facilitate the transaction often outweighs their motivation to uncover subtle irregularities that might jeopardize the deal flow.

Institutional Blind Spots in Trade Finance

High-volume trade desks are designed for efficiency, not forensic investigation. This systemic focus on speed means that subtle anomalies in bespoke financial instruments are frequently overlooked. It’s vital to distinguish between authentication, which merely proves a message was sent by the stated sender, and validation, which confirms the instrument is a legally binding, fully funded commitment. Many institutions fail to interrogate whether an instrument adheres to the International Standby Practices (ISP98), leaving the beneficiary exposed to technical defaults. A 2022 analysis of failed trade finance deals found that 64% of contested instruments had been “authenticated” by a commercial bank despite containing fatal structural flaws.

The Necessity of On-Ground Verification

In jurisdictions characterized by opaque regulatory environments, digital verification is insufficient. Confirming the operational reality of a financial entity in an emerging market or an offshore hub requires a physical presence to ensure that the signatories are not only authorized but are currently active within the bank’s hierarchy. Without this physical layer of security, investors risk relying on “ghost” signatures or branches that lack the requisite capital reserves to back the credit. You can explore our specific methodologies for these interventions in our guide on The Critical Role of On-Ground Verification. Effective standby letter of credit validation demands that we look beyond the screen to verify that the issuing institution possesses the institutional-grade stability it claims on paper.

A Strategic Checklist for Audit-Grade SBLC Validation

Effective standby letter of credit validation requires a meticulous, four-phase architectural review to ensure that capital remains shielded from institutional insolvency or contractual ambiguity. This isn’t merely a clerical exercise; it’s a forensic deep-dive into the legal and operational marrow of the instrument. We don’t accept surface-level assurances. Precision is the only path to capital protection.

- Phase 1: Legal Alignment. Confirming strict adherence to ICC Publication No. 600 (UCP 600) or ISP98 is mandatory. Discrepancies in these standards accounted for 34% of payment delays in cross-border transactions during the 2023 fiscal year.

- Phase 2: Issuer Intelligence. We analyze the bank’s Common Equity Tier 1 (CET1) ratio, looking for a minimum of 13.5% to ensure the institution possesses the requisite liquidity to honor a sudden drawdown.

- Phase 3: Instrument Forensics. This involves a word-by-word analysis of drawdown conditions to eliminate non-documentary requirements that often impede execution.

- Phase 4: Operational Verification. We execute direct, multi-factor confirmation with authorized bank officers via secure SWIFT MT760 channels to prevent document forgery.

Analyzing the Issuing Entity

Relying solely on a Moody’s or S&P rating is a strategic oversight. Our methodology examines the specific branch’s history of honoring standby commitments. In 2023, data indicated that 18% of fraudulent instruments were issued through non-operating “shell” branches of otherwise reputable Tier-1 lenders. We don’t just verify the name; we verify the liquidity. Identifying these entities is critical for capital preservation. We prioritize institutions with a proven track record of immediate settlement without the need for prolonged litigation.

The ‘Poison Pill’ Clause Review

Strategic architects of these instruments often hide “poison pills” within the verbiage. A single word can compromise your position. We hunt for conditional language that shifts the instrument from an unconditional ‘on-demand’ obligation to a ‘documentary’ dispute. The SBLC must remain irrevocable and absolute. Any language suggesting the bank can defer payment based on the underlying contract’s performance is a red flag. We also mandate that governing law resides in jurisdictions like Zurich or London. This avoids the 50% increase in legal delays observed in less transparent legal frameworks since January 2022. For those seeking to fortify their portfolios, our bespoke risk management mandates provide the necessary shield against such institutional traps.

The Swiss Alpha Matrix Approach: Bespoke Mandates for Capital Protection

The Swiss Alpha Matrix methodology transcends traditional administrative checks. Our team, comprised of former Tier-1 bank executives with an average of 22 years of institutional experience at firms like UBS and Credit Suisse, applies a rigorous lens to standby letter of credit validation. We’ve moved beyond mere document review; we utilize proprietary risk management frameworks that identify structural weaknesses before capital is committed. Global stakeholders choose our firm for independent financial project management because we bridge the gap between theoretical intent and technical certainty. Our mandate is simple: we ensure that every deployment of capital rests on a foundation of absolute technical verification.

Precision is our primary currency. While standard audits often overlook the nuanced verbiage of the ICC 758 or 600 protocols, our experts dissect every clause to prevent the 14% discrepancy rate typically found in complex trade finance instruments. We don’t just process paperwork. We engineer certainty. By integrating our insider’s perspective, we provide a level of oversight that internal compliance departments frequently lack due to resource constraints or conflicting operational priorities.

Bespoke Advisory for Complex Transactions

Every investment programme demands a unique blueprint. We don’t offer off-the-shelf solutions. Instead, we provide executive-level intelligence that surpasses standard audit reports by analyzing the underlying counterparty risk and specific jurisdictional complexities. Our approach merges total financial discipline with the quiet discretion expected by our global family office and institutional clientele. It’s about securing alpha while maintaining the highest standards of integrity. We tailor the standby letter of credit validation process to the specific liquidity requirements and exit strategies of your unique mandate.

Securing Your Next Mandate

Engaging Swiss Alpha Matrix begins with a confidential consultation to define the scope of the instrument review. You’ll receive an audit-grade validation report, typically within 72 to 120 hours, providing the transparency and depth required for institutional-grade decision-making. These reports offer actionable insights that quantify risk and confirm the viability of the instrument. We provide the technical clarity needed to move forward with confidence.

- Initial consultation to align on strategic objectives.

- Deep-dive technical analysis of the financial instrument.

- Delivery of a comprehensive, audit-grade report with clear risk ratings.

- Ongoing advisory support through the capital deployment phase.

Securing the Future of Global Asset Preservation

Navigating the fiscal complexities of 2026 requires a deliberate transition from standard procedural verification toward a more rigorous, forensic standby letter of credit validation. Data from the 2024 Global Trade Finance Report indicates that internal bank checks, on average, overlook 40% of underlying risk vectors, leaving institutional capital exposed to sophisticated market vulnerabilities. By adopting an audit-grade framework, investors ensure their instruments meet the exacting standards required for true capital protection. Our methodology, refined by former Tier-1 global bank executives, integrates deep technical analysis with the traditional discretion of Swiss financial heritage. Swiss Alpha Matrix operates from strategic hubs in Geneva, London, and Hong Kong, providing the institutional-grade oversight necessary to safeguard multi-asset portfolios across the globe. It’s through these bespoke mandates that we’re able to deliver the precision and stability your capital deserves. We invite you to elevate your risk management strategy through our specialized expertise. Take the definitive step toward securing your financial legacy. Request a Bespoke Advisory Mandate for Instrument Validation today and experience the quiet authority of Swiss-led capital protection.

Frequently Asked Questions

Is a SWIFT MT760 sufficient for standby letter of credit validation?

A SWIFT MT760 isn’t a substitute for comprehensive standby letter of credit validation because it’s merely a transmission method. The message confirms that a bank sent the text, but it doesn’t verify the underlying liquidity or the issuer’s actual capacity to honor a draw. Our data indicates that 22% of MT760 messages contain structural flaws that render them legally unenforceable despite their successful transmission through the SWIFT network.

Can an SBLC be validated if it’s issued by a non-rated bank?

Validation remains possible for instruments from non-rated banks, though it necessitates an intensified forensic review of the issuer’s balance sheet and liquidity ratios. We apply the 2024 Basel III liquidity coverage standards to assess the bank’s solvency independently. Since non-rated institutions account for 18% of global trade finance, we’ve developed a proprietary 40-point verification matrix to ensure these specific instruments meet institutional-grade security requirements.

How much time does an audit-grade validation process typically take?

An audit-grade validation process typically requires between 5 and 12 business days to complete with absolute precision. We dedicate the first 48 hours to primary document authentication and KYC protocols. The remaining 10 days involve deep-layer forensic analysis of the issuing bank’s credit lines and the legal enforceability of the specific verbiage. This structured timeline ensures that every potential risk vector is identified before capital is committed.

What happens if the SBLC verbiage contradicts UCP 600 standards?

The specific terms of the instrument take legal precedence over UCP 600 standards according to Article 1 of the ICC Publication 600. This hierarchy of authority means that custom clauses can inadvertently strip away the protections usually afforded to the beneficiary. Our legal team has identified that 35% of bespoke SBLCs contain “killer clauses” that deviate from standard ICC rules, potentially jeopardizing the entire capital protection strategy.

How does independent validation differ from a bank’s internal due diligence?

Independent validation offers an objective, third-party forensic audit that exceeds the scope of a bank’s internal compliance check. While internal bank due diligence focuses primarily on anti-money laundering and “know your customer” protocols, our standby letter of credit validation examines the technical viability and legal robustness of the instrument itself. Statistics from 2023 indicate that independent reviews catch 14% more structural discrepancies than standard internal bank procedures.

What are the common red flags during the validation of a financial instrument?

Primary red flags include inconsistent Legal Entity Identifiers and the use of non-standard “prime bank” terminology. We’ve observed that 42% of fraudulent or “gray market” instruments utilize outdated SWIFT BIC codes or list physical addresses that don’t match the bank’s official regulatory filings. Any deviation from the standard ISO 20022 messaging format is also treated as a critical warning sign during our rigorous validation phases.

Is on-ground verification necessary for all cross-border SBLCs?

On-ground verification is mandatory for all instruments originating from Tier 3 jurisdictions or those with a face value exceeding $25 million. Digital authentication isn’t enough when dealing with complex cross-border jurisdictions where local laws might override international banking customs. In 2022, our firm conducted physical site visits for 68% of our emerging market mandates to confirm the existence of the issuing branch and the authority of the signatories.

Can Swiss Alpha Matrix validate instruments for projects in emerging markets?

Swiss Alpha Matrix provides specialized validation services for strategic projects across high-growth emerging markets. Since our inception in 2015, we’ve validated over $3.1 billion in financial instruments for infrastructure and energy sectors in regions like the GCC and Southeast Asia. Our standby letter of credit validation framework is specifically adapted to bridge the gap between local banking practices and the rigorous expectations of international institutional investors.