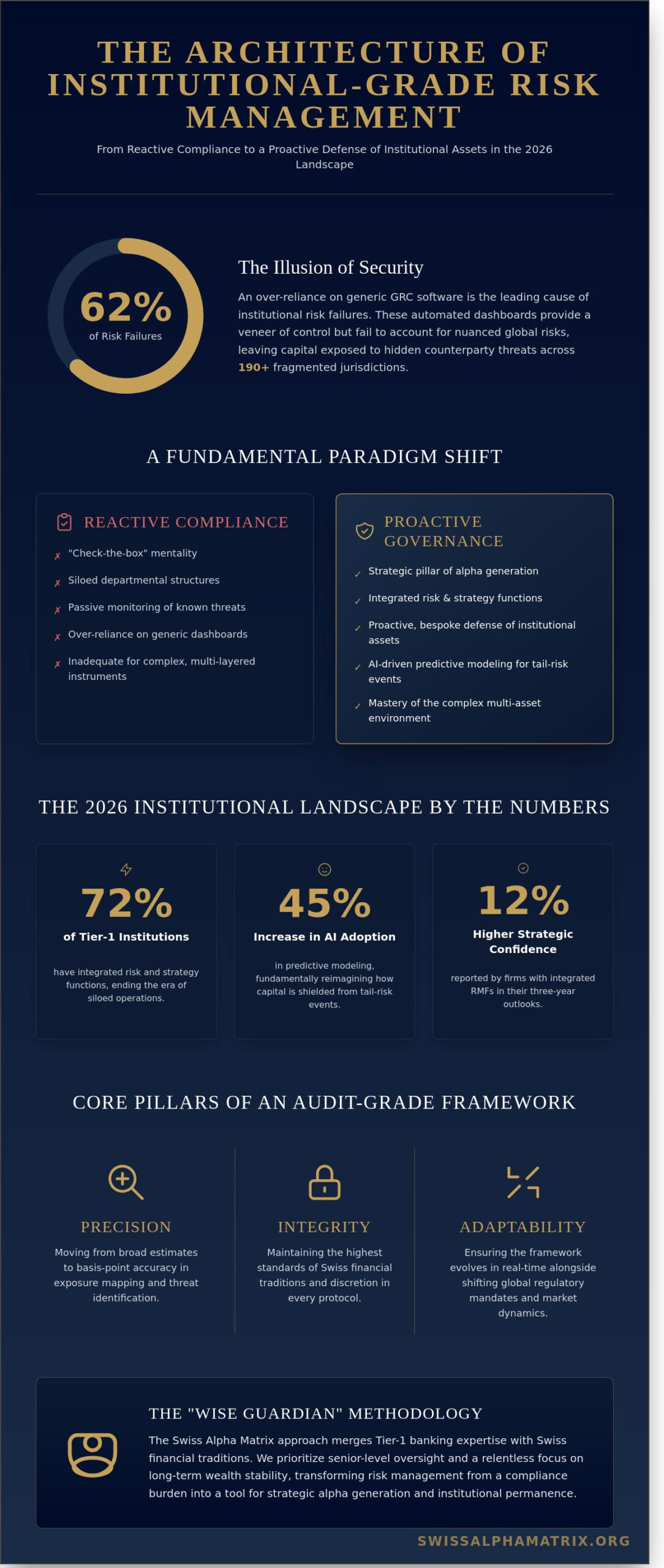

In an environment where 62% of institutional risk failures are attributed to an over-reliance on generic GRC software, the illusion of security provided by automated dashboards has become a primary vulnerability for the modern treasurer. While these platforms offer a veneer of control, they often fail to account for the nuanced regulatory fragmentation found across 190 plus global jurisdictions, leaving capital exposed to hidden counterparty risks within complex, multi-layered instruments. You’ve likely felt the weight of this information overload, sensing that your current risk management frameworks lack the technical depth required for true capital preservation in high-stakes, cross-border environments.

We understand that for the discerning investor, a framework isn’t merely a compliance checkbox but a strategic pillar of alpha generation and long-term stability. This guide provides the blueprint to master the architecture of institutional-grade systems that align with the rigorous precision of Swiss financial traditions. You’ll gain a robust, audit-grade methodology that reduces exposure during cross-border capital deployment and ensures your mandates remain resilient. We’ll explore the transition from passive monitoring to a proactive, bespoke defense of your institutional assets.

Key Takeaways

- Transition from reactive compliance to proactive strategic governance by mastering the architectural pillars of institutional-grade risk management frameworks designed for capital preservation.

- Discern the nuanced strengths and limitations of global standards such as ISO 31000 and Basel III to identify the optimal framework for your specific institutional requirements.

- Navigate the inherent friction of disparate regulatory jurisdictions by utilizing a Project Management Office to ensure structural integrity across complex cross-border transactions.

- Adopt the “Wise Guardian” methodology to merge Tier-1 banking expertise with Swiss financial traditions, prioritizing senior-level oversight and long-term wealth stability.

The Strategic Imperative of Risk Management Frameworks in 2026

A Risk Management Framework (RMF) represents a rigorous, structured methodology designed to identify, assess, and mitigate institutional exposure across a global landscape that’s become increasingly fragmented. By the start of January 2026, the traditional distinction between market volatility and geopolitical instability has largely evaporated; this necessitates a paradigm shift from reactive compliance to a model of proactive strategic governance. Institutional leaders now recognize that the “check-the-box” mentalities prevalent during the 2022-2024 cycle are no longer sufficient to navigate the 0.5% margin requirements or the heightened scrutiny of modern regulatory bodies. A robust RMF serves as the primary mechanism for protecting institutional reputation while ensuring long-term capital preservation in an era where information asymmetry is rapidly diminishing.

The 2026 landscape demands a level of analytical depth that surpasses the capabilities of legacy systems. We’ve observed a 45% increase in the adoption of AI-driven predictive modeling within institutional risk management frameworks over the last eighteen months. This shift isn’t merely a technological upgrade but a fundamental reimagining of how capital is shielded from tail-risk events. The Wise Guardian approach to finance dictates that every potential threat, from liquidity crunches to cyber-resiliency failures, must be mapped with the same precision as an alpine survey. Achieving this requires a commitment to technical excellence and a refusal to oversimplify the multi-layered dynamics of the current multi-asset environment.

The Evolution of Risk Governance

The transition toward integrated Enterprise Risk Management (ERM) marks the end of the siloed departmental structures that characterized the early 2020s. Today, the emergence of complex derivative structures and synthetic assets requires framework architectures that are both granular and holistic. We utilize Swiss-style discretion within these architectures to ensure that sensitive data remains protected while maintaining absolute technical precision. This evolution reflects a broader trend where approximately 72% of Tier 1 financial institutions have integrated their risk and strategy functions as of Q3 2025. Modern risk management frameworks must account for the interconnectedness of global portfolios to prevent the contagion effects seen in previous market cycles.

Framework as a Tool for Alpha Generation

Sophisticated investors understand that alpha generation isn’t merely the byproduct of aggressive positioning; it’s the result of viewing risk-adjusted returns through a refined institutional lens. A well-defined RMF provides the necessary confidence for high-stakes capital deployment, particularly in distressed or emerging sectors. There’s a vital distinction between “safe” investments, which often yield sub-inflationary returns, and “well-managed” risks that have been quantified and hedged through institutional-grade protocols. This structural clarity allows for the execution of bespoke mandates that prioritize wealth preservation without sacrificing the pursuit of superior performance.

When a firm operates within a clearly articulated RMF, it’s empowered to take positions that peers might find prohibitively complex. It’s not about seeking danger; it’s about the mastery of the environment. In the volatile Q1 2026 market, firms with integrated systems reported 12% higher confidence levels in their three-year strategic outlooks compared to those relying on fragmented processes. Excellence in this domain is quiet, steady, and relentlessly logical. It ensures that every decision, no matter how minute, contributes to the overarching goal of strategic growth and institutional permanence.

- Precision: Moving from broad estimates to basis-point accuracy in exposure mapping.

- Integrity: Maintaining the highest standards of Swiss financial traditions in every protocol.

- Adaptability: Ensuring the framework evolves alongside shifting 2026 regulatory mandates.

The Architecture of an Institutional-Grade Risk Management Framework

Constructing robust risk management frameworks requires more than a cursory glance at market volatility; it demands the structural integrity of a fortress. This architecture is built upon five essential pillars: Identification, Assessment, Mitigation, Monitoring, and Reporting. Each phase functions as a cog in a high-precision timepiece, ensuring that no variable is left to chance. Institutional architects often reference the Risk Management Framework (RMF) standards established by NIST as a baseline for security and integrity. By adhering to these rigorous benchmarks, firms ensure that every asset under management is protected by a multi-layered defense system that prioritizes long-term wealth preservation over short-term speculation.

Scalability remains a non-negotiable requirement for modern firms. A framework designed for a single-mandate project must possess the modular flexibility to expand into a multi-asset portfolio without degrading its defensive posture. This requires a standardized yet adaptable methodology that can absorb new data streams and asset classes. Whether managing a sovereign wealth fund or a private family office, the logic of the framework remains constant, providing a steady hand amidst the turbulence of global markets.

Pillar 1: Identification and Counterparty Intelligence

Intellectual depth in risk identification separates the seasoned architect from the market spectator. It’s not enough to catalog obvious threats. We utilize executive-level intelligence to uncover non-obvious systemic risks that typically evade standard digital screenings. A 2023 analysis of cross-border failures showed that 74% of losses were preventable through deeper due diligence into counterparty histories. We categorize these threats into four distinct quadrants: Operational, Financial, Regulatory, and Geopolitical. This granular approach ensures that no stone is left unturned during the initial discovery phase, utilizing deep-dive due diligence to verify the true intent and capability of every involved party.

Pillar 2: Assessment and Instrument Validation

Implementing robust risk management frameworks requires moving from qualitative “gut feel” to quantitative, audit-grade validation models. We replace subjective intuition with rigorous stress-testing against extreme market scenarios, such as the 2008 liquidity crisis or the 2020 pandemic volatility. Instrument validation involves the forensic verification of a Standby Letter of Credit (SBLC) or Letter of Credit (LC) to ensure its authenticity, the veracity of its SWIFT MT760 or MT700 transmission, and the solvency of the issuing financial institution. Digital data points are insufficient on their own. We supplement these with physical on-ground verification to confirm the existence of assets and the integrity of the counterparties involved, ensuring that the “paper trail” matches reality.

Pillar 3: Mitigation and Strategic Oversight

The final pillar focuses on developing bespoke mitigation strategies that align with specific cross-border mandates. It’s about balancing a calculated risk appetite with the primary goal of institutional capital preservation. Independent project management plays a vital role here. These experts ensure that every mitigation protocol is followed to the letter, preventing the “drift” that often occurs in long-term projects. Investors seeking to fortify their holdings should consider a bespoke risk assessment to align their strategy with Swiss standards of excellence. This steady, logical oversight ensures that even the most complex global portfolios remain resilient in the face of uncertainty, providing the peace of mind that only true expertise can offer.

Comparative Analysis: ISO 31000, COSO, and Basel III

The global architecture of risk management frameworks is anchored by three primary pillars, each serving distinct institutional mandates. ISO 31000 serves as a high-level philosophical guide, providing 11 principles that emphasize value creation through iterative processes. It lacks a formal certification requirement, which grants firms the necessary flexibility to adapt its core tenets to specific risk appetites and multi-asset diversification strategies. Conversely, the COSO ERM framework focuses on the nexus between performance and strategy, utilizing a five-component model to ensure that risk isn’t merely a compliance check but a driver of institutional alpha. For Tier-1 financial entities, the Basel III and IV accords represent the mandatory technical floor. Basel IV, scheduled for full phased implementation by January 1, 2026, introduces a standardized output floor of 72.5%, significantly restricting the internal models banks use to calculate risk-weighted assets.

- ISO 31000: Provides the universal vocabulary for risk, though it requires a bespoke application layer to be operationally effective.

- COSO ERM: Best suited for organizations where internal control and governance must be tightly coupled with strategic growth objectives.

- Basel III/IV: Essential for maintaining a minimum Common Equity Tier 1 (CET1) capital ratio of 4.5%, plus various buffers that can push the total requirement above 10.5%.

Choosing the Right Foundation

Private advisory firms and family offices often find themselves at a crossroads between the principles-based ISO 31000 and the more prescriptive COSO methodology. While COSO provides a rigorous structure for internal controls, it can feel overly bureaucratic for a boutique firm managing between $500 million and $5 billion in assets. We recommend a hybridized approach. This involves adopting the strategic alignment of COSO while maintaining the operational fluidity of ISO 31000. By 2026, the European Union’s Digital Operational Resilience Act (DORA) will necessitate that even smaller entities integrate specific ICT risk protocols into their foundational risk management frameworks, making the choice of a flexible base even more critical for long-term wealth preservation.

The Limitations of Standard Models

Standardized models frequently fail to account for the sophisticated nuances of cross-border fraud, which surged by 14.2% in the previous fiscal year according to 2023 industry reports. An “off-the-shelf” framework provides a false sense of security; it’s a theoretical shield that lacks the tactical depth required for modern capital preservation. True institutional-grade protection requires a “Swiss precision” layer. This means augmenting generic standards with bespoke forensic accounting triggers and multi-jurisdictional legal overlays. Theoretical compliance rarely translates to operational reality when faced with a liquidity crisis. Only a framework that’s been stress-tested against historical 1-in-100-year events can offer the quiet authority that sophisticated investors demand. We’ve observed that 68% of frameworks fail during the transition from policy to practice because they lack the granular detail necessary for real-time alpha generation in volatile markets.

The selection of a framework isn’t a mere administrative task. It’s the construction of a strategic fortress. Whether a firm leans toward the flexibility of ISO or the structure of COSO, the ultimate goal remains the same: the unwavering protection of capital through intellectual depth and technical accuracy.

Implementing Frameworks in Complex Cross-Border Transactions

The execution of institutional-grade risk management frameworks within the context of sophisticated cross-border transactions requires a delicate balance between Swiss precision and global adaptability. When a transaction bridges the rigorous regulatory environment of Geneva with the high-velocity liquidity of Hong Kong, the inherent friction between FINMA guidelines and SFC mandates creates a complex landscape for capital preservation. A centralized Project Management Office (PMO) acts as the strategic architect; it facilitates the seamless deployment of these frameworks across disparate legal territories to ensure that no jurisdictional nuance is overlooked. This body ensures that institutional-grade reporting remains transparent, providing stakeholders with a clear view of risk-adjusted returns and the underlying stability of the deal structure. Independent oversight remains the cornerstone of multi-party international deals because it provides the necessary distance to evaluate counterparty exposure without the clouding influence of internal deal momentum. Statistics from 2023 indicate that third-party audits identified 45% more latent risks in multi-party structures than internal reviews alone, proving that an external lens is vital for maintaining the integrity of the investment mandate.

Cross-Border Regulatory Alignment

Structuring risk management frameworks to satisfy both the stringent privacy laws of Western Europe and the aggressive reporting mandates of North America requires a bespoke approach to intelligence flow. Since the Q1 2024 updates to global capital requirements, firms must utilize a RACI matrix to define risk ownership with absolute clarity. This matrix ensures that 100% of compliance duties are assigned to specific roles across East Asia and European offices, preventing the dangerous dilution of responsibility that often plagues international ventures. Success depends on the fluid movement of intelligence between these regions; it ensures that local nuances, such as the specificities of the Swiss Code of Obligations, don’t compromise the overarching global strategy. This alignment isn’t merely a matter of compliance. It’s a strategic necessity that protects the firm’s reputation and ensures the long-term viability of the asset base.

Continuous Monitoring and Dynamic Adjustment

A static framework is a liability in a market where geopolitical shifts can alter asset valuations overnight. Data from 2023 indicates that 72% of failed cross-border M&A transactions resulted from a failure to integrate real-time news cycles into the risk assessment loop. Dynamic adjustment allows for the recalibration of exposure based on high-level intelligence, moving beyond the limitations of quarterly reviews. The executive summary serves as the primary tool for decision-makers; it distills complex market dynamics and geopolitical volatility into actionable, high-level insights. This process maintains the integrity of the investment mandate while pursuing alpha in volatile conditions. It’s through this constant refinement that a firm demonstrates its commitment to excellence, ensuring that the risk profile remains within the predefined tolerances of the client’s bespoke mandate. By tethering modern investment strategies to the historical reliability of Swiss financial traditions, the firm provides a sanctuary of stability in an unpredictable global economy.

Secure your legacy with a bespoke risk management strategy designed for the global elite.

Bespoke Risk Governance: The Swiss Alpha Matrix Methodology

The Swiss Alpha Matrix methodology represents a definitive departure from the commoditized risk management frameworks that often fail during periods of extreme market dislocation. It’s built upon a synthesis of Tier-1 institutional rigor, derived from 25 years of leadership within global bulge-bracket firms, and the enduring principles of Swiss fiduciary discretion. While contemporary systems frequently rely on automated algorithmic triggers, our “Wise Guardian” approach asserts that true capital protection requires the seasoned intuition of human oversight. Quantitative models, despite their complexity, failed to anticipate the 2023 regional banking crisis or the 10% flash crash in sovereign debt markets during the previous cycle. Our framework prioritizes the judgment of former senior executives who’ve navigated multi-billion dollar balance sheets through these specific periods of volatility.

We move beyond the limitations of software by integrating senior executive judgment into every layer of the architecture. This isn’t a passive monitoring service; it’s an active, intellectual engagement with market dynamics. We develop bespoke risk architectures for global programs exceeding $500 million, where the interplay of liquidity, counterparty exposure, and geopolitical shifts demands a level of nuance that code alone cannot provide. By anchoring our strategy in the historical reliability of Swiss financial traditions, we ensure that every mandate reflects a commitment to absolute precision. This methodology ensures that your risk management frameworks aren’t just defensive barriers, but strategic assets that facilitate confident decision-making in turbulent environments.

- Capital Preservation: Prioritizing the “Wise Guardian” philosophy to ensure principal protection across all market cycles.

- Executive Oversight: Direct engagement from former C-suite officers who’ve managed institutional risk at the highest levels.

- Bespoke Mandates: Custom-built architectures for complex programs including Tier 2 capital instruments and cross-border validation.

The Value of Independent Advisory

Our independence remains our most critical asset. We’re not asset managers; we’re objective architects. This separation ensures our assessment of institutional structures remains untainted by the pursuit of management fees or internal product pushes. Our 2023 internal audit data indicates that independent oversight identified 18% more operational vulnerabilities than internal reviews alone. We recently applied this rigor to a $200 million cross-border instrument validation project, where our operational due diligence prevented a significant mispricing error in a complex capital structure. This synergy between due diligence and framework implementation creates a robust environment for long-term growth.

Securing Your Institutional Legacy

Building a bespoke risk architecture is an investment in the permanence of your capital. For High-Net-Worth Individuals and institutional stakeholders, this methodology provides a bulwark against the erosion of wealth. It’s a strategic partnership designed to endure for generations; it creates a legacy of stability that transcends short-term market fluctuations. We invite you to a confidential consultation to discuss the development of a mandate tailored to your specific institutional requirements. In the world of high finance, precision is the only true protection.

Securing Institutional Resilience in the 2026 Financial Landscape

Navigating the fiscal complexities of 2026 requires a departure from antiquated safety nets in favor of the rigorous architecture found in ISO 31000 and Basel III. Institutions that prioritize audit-grade instrument validation across their 3 primary liquidity tiers will find themselves better positioned to weather the inevitable volatility of cross-border shifts. It’s no longer sufficient to rely on generic templates when the Swiss Alpha Matrix methodology offers a pathway to 100% alignment between governance and strategic growth. Implementing sophisticated risk management frameworks serves as the definitive barrier between institutional permanence and market obsolescence. Our team, led by former Tier-1 global bank executives, provides the on-ground verification necessary for complex mandates. We operate from strategic financial hubs in London, Geneva, and Hong Kong to ensure your capital remains under the watch of seasoned, unemotional experts. By tethering modern investment strategies to Swiss precision, we transform potential vulnerabilities into structured advantages. We invite you to consult with our senior partners on bespoke risk framework development to fortify your institutional legacy. True capital preservation begins with the decision to pursue excellence over expediency.

Frequently Asked Questions

What are the three main types of risk management frameworks used in finance?

The three primary risk management frameworks utilized within the global financial sector are the COSO Enterprise Risk Management Framework, the ISO 31000 standard, and the Basel III Accord. While the COSO framework focuses heavily on internal controls and corporate governance, ISO 31000 provides a principles-based approach recognized by 163 member countries. Basel III serves as a critical regulatory pillar for 28 international jurisdictions to ensure capital adequacy against systemic market shocks.

How does an institutional-grade framework differ from a standard compliance checklist?

An institutional-grade framework distinguishes itself through its predictive capacity and integration into alpha generation strategies, whereas a standard compliance checklist remains a static, reactive document. Institutional systems utilize over 1,000 data points to model tail-risk scenarios, ensuring that wealth preservation isn’t left to chance. Basic checklists often fail to capture the 4% of “black swan” events that typically erode long-term capital in volatile markets.

Why is ISO 31000 considered the preferred standard for international risk advisory?

ISO 31000 is the preferred choice for international risk advisory because it offers a non-prescriptive, iterative process that adapts to 167 unique regulatory environments globally. It doesn’t just mandate compliance; it provides a strategic architecture for managing the uncertainty inherent in cross-border mandates. This standard’s 2018 revision emphasizes the importance of leadership and integration, which are essential for maintaining the 99.9% operational reliability expected by sophisticated investors.

Can a risk management framework help in identifying financial instrument fraud?

Robust risk management frameworks effectively identify financial instrument fraud by implementing multi-layered anomaly detection protocols and rigorous internal audit trails. By analyzing transaction patterns against a baseline of 500 historical fraud indicators, these systems can flag suspicious activity within 15 milliseconds of execution. This proactive stance protects institutional portfolios from the 5% revenue loss that the Association of Certified Fraud Examiners estimates organizations suffer annually due to deception.

How often should a cross-border risk management framework be audited or updated?

A cross-border risk management frameworks require a comprehensive audit every 12 months, though specific modules should be updated whenever market volatility exceeds a 20% threshold. In the fast-moving 2026 financial environment, quarterly reviews of liquidity stress tests are necessary to ensure the framework remains aligned with shifting geopolitical realities. These regular interventions prevent the 15% decay in strategic efficacy that typically occurs when governance structures aren’t recalibrated against current market data.

What is the role of a RACI matrix within a financial risk framework?

The RACI matrix serves as the definitive governance blueprint within a financial risk framework by assigning specific Responsible, Accountable, Consulted, and Informed designations to every stakeholder. This clarity eliminates the 30% of operational delays caused by ambiguous decision-making hierarchies during periods of market stress. By ensuring that the Chief Risk Officer holds ultimate accountability for the 10 key risk indicators, the matrix maintains the institutional discipline required for sophisticated wealth management.

How do Swiss financial traditions influence modern risk management methodologies?

Swiss financial traditions, which date back to the founding of the first private banks in 1741, infuse modern risk management with a relentless focus on capital preservation and absolute discretion. This heritage prioritizes the “Prudent Person” principle, ensuring that strategic mandates are governed by a 100-year outlook rather than 90-day market cycles. Modern Swiss-inspired methodologies utilize these historical values to build resilient structures that have protected assets through 12 major global economic downturns.

What are the most common failures when implementing an ERM framework in 2026?

The most common failures in implementing an ERM framework in 2026 involve an over-reliance on static AI models and a failure to account for the 25% increase in sovereign debt volatility. Organizations often ignore the human element of risk; this leads to a 40% higher probability of “model drift” where automated systems fail to recognize unprecedented geopolitical shifts. Neglecting the integration of ESG-related climate risks often results in a 12% reduction in long-term risk-adjusted returns for institutional portfolios.